Resources for mortgage relief

Americans everywhere are suffering financially due to COVID-19 outbreak. If you or your family is struggling to make your monthly mortgage payment because of the COVID-19 pandemic there is help available. Help is being offered to the average homeowner by the Federal Government, State Government, as well as specific lenders. This help comes in the form of payment programs, forbearance, loan modifications, and other ways to reduce the financial burden of your monthly mortgage payments.

The Consumer Financial Protection Bureau (CFPB) offers insightful information regarding Mortgage Relief Options related to COVID-19.

Skip to

Federal mortgage relief programs

March 27, 2020 the CARES Act was signed into law. CARES is an acronym for Coronavirus Aid, Relief and Economic Security Act. The goal of this law that has taken place is to provide $2 trillion dollars in economic relief for American consumers impacted by COVID.

Here are some important aspects of the CARES Act…

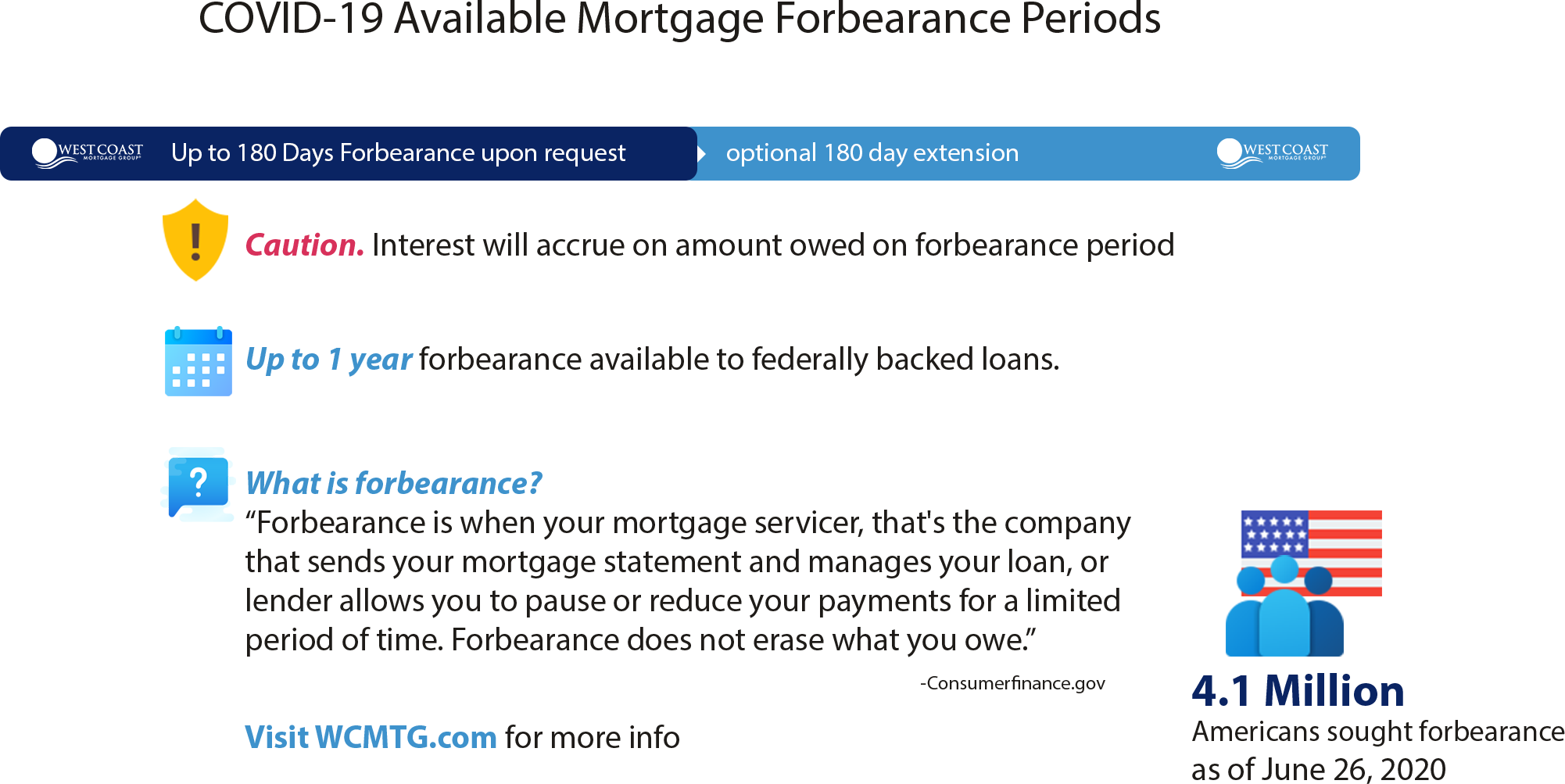

- Applies to federally backed mortgages, which include conventional loans funded by Fannie Mae, Freddie Mac, FHA, USDA, and VA

- Gives borrower the right to request a forbearance for up to 180 days with an optional extension of an addition 180 days

- You may be able to freeze additional fees during the forbearance period

- The suspension of negative credit reporting for borrowers who were current on payments before their forbearance.

Payment deferral option by Fannie Mae and Freddie Mac

An announcement was made May 13, 2020 by the government-sponsored enterprises Fannie Mae and Freddie Mac. They announced that COVID-19 Payment Deferrals will be an available option to borrowers who own a federally backed mortgage starting July 1st.

FANNIE MAE COVID MORTGAGE RELIEF

Due to the CARES Act, Fannie Mae may qualify you for the following mortgage relief options…

- Ability to suspend mortgage payments for up to one year

- Suspension of late fees during the forbearance period

- Various repayment plans post forbearance, these payment plans include gradual repayment or loan modification

FREDDIE MAC

- Provides forbearance for up to a year

- Suspension of late fees during the forbearance period

- You may request a loan modification after forbearance or maintain a previous mortgage

Post Mortgage Forbearance Note: Borrowers who made 3 consecutive on-time payments after forbearance are eligible to refinance their home or qualify for a new mortgage.

GIVE US A CALL AND WE WILL ANSWER YOUR COVID-19 MORTGAGE RELATED QUESTIONS

COVID-19 RELATED MORTGAGE FAQ’s

Enrolling in a forbearance program to pause your mortgage payments is a possibility you may be interested in pursuing. First, let us take a second to define forbearance.

According to consumerfinance.gov, forbearance is when your mortgage servicer or lender allows you to temporarily pay your mortgage at a lower payment or pause paying your mortgage. You will have to pay the payment reduction or the paused payments back later.

The short answer is yes.

You may want to consider the fact that the payments that were paused or reduced will be due in one lump sum payment when your normal mortgage payments resume. In addition, interest on the paused or reduced payments will continue to accrue until you repay them.

Reach out to your mortgage lender servicer and ask them what forbearance options are available for your specific loan. It is important to ask this because there are certain stipulations that may qualify or disqualify you from COVID-19 mortgage assistance (forbearance).

Your servicer may allow you to pause payments for one year. The amount throughout this forbearance period is repaid by either adding it to the end of your mortgage loan or by taking out a completely separate mortgage loan.

You may be eligible for a repayment plan where your servicer will add part of your past-due forbearance amount into your regular mortgage payment each month.

There is also deferral or partial claim This means that your servicer may offer to set all or part of your loan’s past-due amount aside to be paid at a later time.

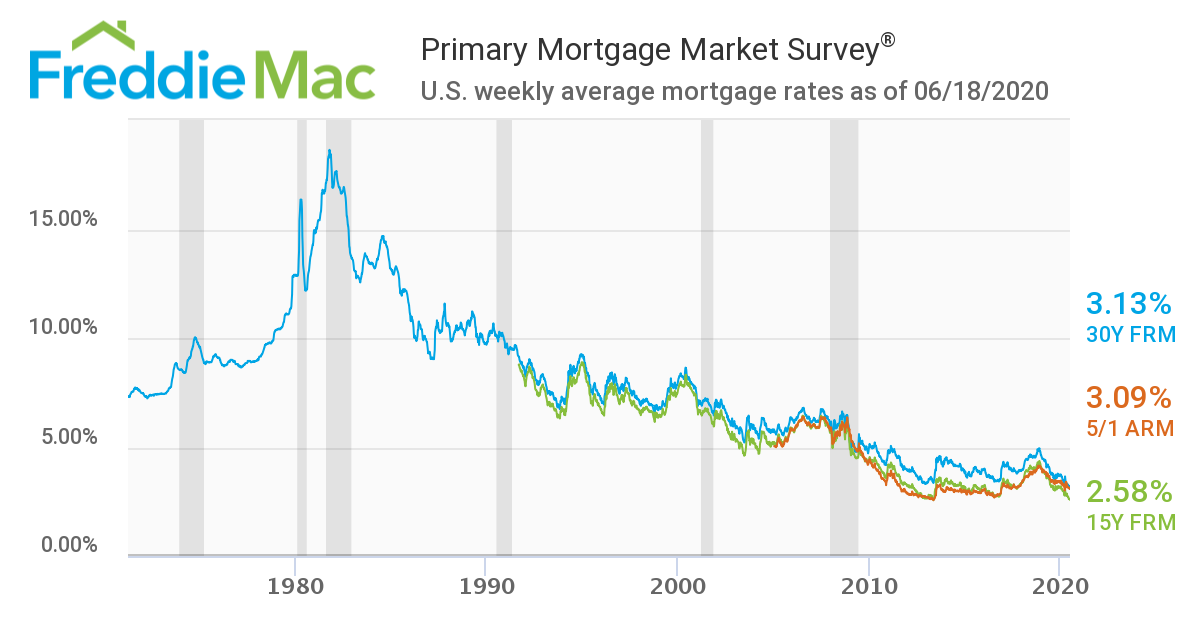

Since the COVID-19 Pandemic began, mortgage rates have decreased to new lows. According to Freddie Mac, mortgage rates are at an all-time low. *The Federal Home Loan Mortgage Corporation, known as Freddie Mac, is a public government-sponsored enterprise, headquartered in Tysons Corner, Virginia. To put it in perspective, here is a chart that shows the historical mortgage rates (created June 22, 2020).

During the COVID-19 crisis, refinancing your home is generally done under the same guidelines as before.

Have you been let go or furloughed from your job due to COVID-19?

If so you may have a difficult time refinancing your home. Generally, investors that purchase home loans want to see that their applicants are employed and meet a certain set of criteria before they fund a loan.

Are you still employed?

If so, you may be able to enjoy some of the lowest rates in mortgage history. Up to June 24, 2020 we have seen historical lows for the mortgage market. If you have not yet refinanced your home, it may be a good time to consider doing so.

Did you know we can finish your loan from start to finish without you ever having to leave your home? Thanks to email and other forms of electronic communication you never have to physically come into our office to get your loan funded.

What about signing paperwork?

We can send you digital copies of the paperwork that needs signing and you can sign them with an electronic signature. You may also receive physical copies of the paperwork to review and sign after one of our couriers drops it off at your home.